Be a part of the solution

The emerging Israel–U.S.–Iran war is already triggering market reactions, threatening critical global food production systems, especially in sub-Saharan Africa, Asia, the Pacific, and Latin America, in the upcoming major planting seasons. Fertilizer supply has tightened and prices are rising.

Within a week of the conflict escalation, average fertilizer free on board (FOB) prices surged, with urea increasing by 37%.1 Major Middle Eastern fertilizer suppliers, locked in behind the Strait of Hormuz, have halted operations and canceled supply contracts amid uncertainty. Recent airstrikes on Iranian oil depots and refinery infrastructure have further heightened concerns over global energy supply disruptions, pushing benchmark crude prices above $100 per barrel for the first time since 2022.2 Rising energy costs are likely to intensify fertilizer price volatility given the strong link between natural gas, oil markets, and nitrogen fertilizer production.

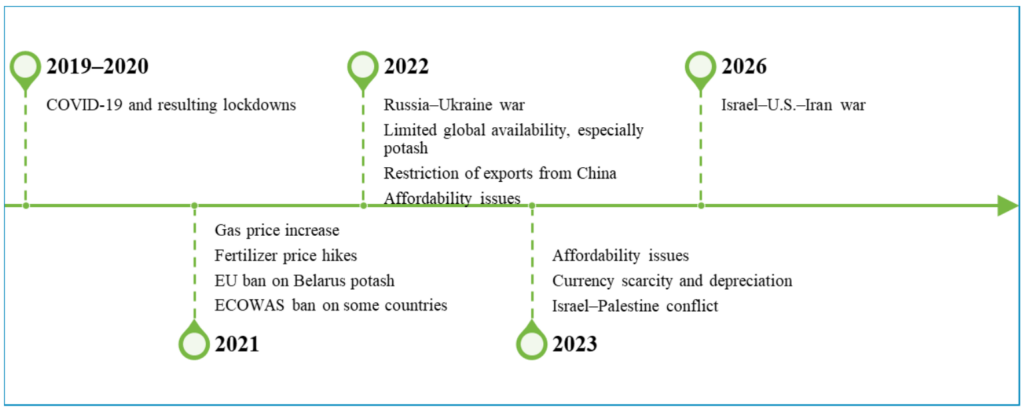

Governments, the private sector, and civil society must act in concert to mitigate the disruption in fertilizer supply chains and guarantee that farmers have timely access to adequate quantities at fair prices. Evidence from the disruptions during COVID-19 and Russian operations in Ukraine demonstrates that proactive regional procurement and coordination mechanisms can cushion supply shocks and stabilize markets. In 2022, the United Nations organized the fertilizer workstream of the Global Crisis Response Group on Food, Energy and Finance. Sustain Africa was launched the same year as a private sector-led response to address the fertilizer crisis on the ground. The current geopolitical escalation requires the same global or regional urgency and coordinated response to mitigate reduced fertilizer use, diminished yields, and increased food prices, building on the learnings from previous crises.

Fertilizers are fundamental to agricultural productivity, production, and global food security, and their demand follows planting calendars that do not adjust to geopolitical instability. Disruptions in their supply generate cascading effects on food systems. Supply shocks trigger price volatility that reduces affordability, while limited availability constrains farmers’ access to essential inputs; as a result, reduced fertilizer application leads to nutrient-deficient soils and lower crop yields, which in turn diminish food supply and inflate consumer food prices.

The impacts are more severe for vulnerable smallholder farmers. In this context, fertilizer is not merely an input but a decisive factor in global food production, often determining whether a season produces surplus or shortage, profit or loss, thereby shaping both household food security and broader market stability.

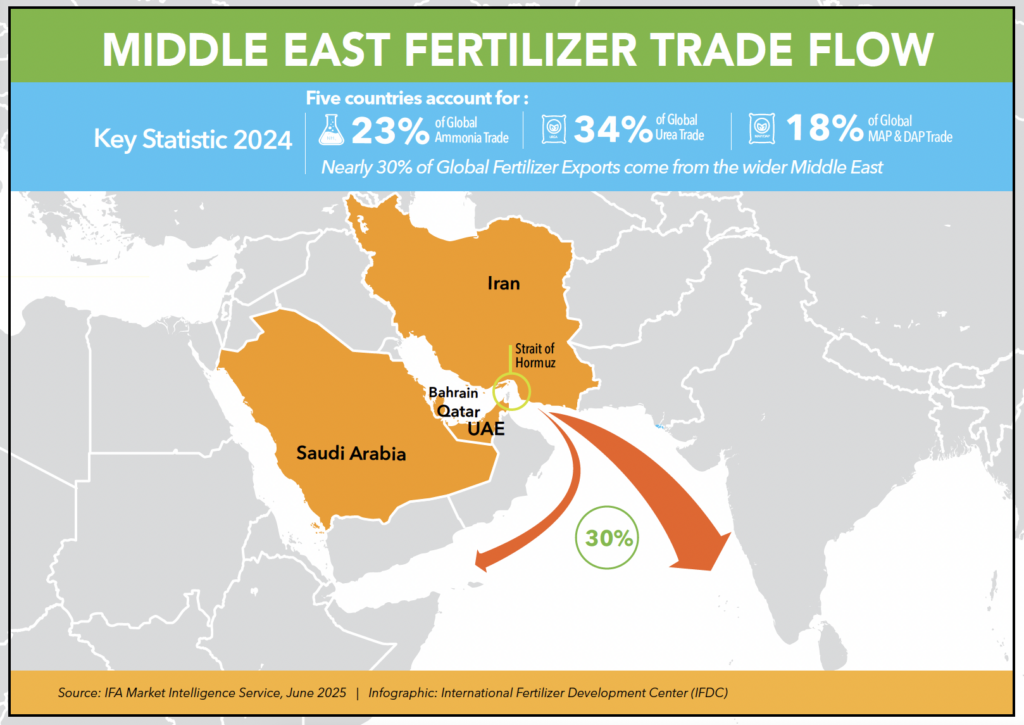

The Middle East accounts for a significant share of global fertilizer exports, with five major exporting countries (Bahrain, Iran, Qatar, Saudi Arabia, and United Arab Emirates) relying on the Strait of Hormuz to transit products to international markets. In 2024, these countries collectively accounted for about 34% of global urea trade, 18% of global monoammonium phosphate (MAP) and diammonium phosphate (DAP) trade, and 23% of global ammonia trade.3

The disruption in production and shipping routes, including higher freight and insurance costs, has already placed additional pressure on global fertilizer supply chains and increased the risk of shortages and price volatility in import-dependent regions. Data from AfricaFertilizer show that between 2020 and 2022, 19% of fertilizers imported into 18 sub-Saharan African countries came from Middle Eastern countries, highlighting the importance of this region for Africa’s fertilizer supply. In 2024, Asian dependence on fertilizers exported from the Persian Gulf exceeded 50%, while the Americas relied on Gulf-exported fertilizer for 18% of its supply.4

Effective fertilizer use depends not only on its availability but also on the timing, predictability, and coordination of supply, since crops require nutrients at specific growth stages to achieve optimal yields. As most countries in sub-Saharan Africa, particularly in West Africa, along with India and Brazil, prepare for the March-April planting season and those in East Africa around June, fertilizers must already be in-country or in transit to importers. Any delay at this stage directly affects planting decisions and harvest outcomes.

Africa remains highly dependent on imported inorganic fertilizers, a structural vulnerability that exposes the continent to global geopolitical shocks. In contrast, Bangladesh and India have expanded domestic production and diversified supply chains, reducing but, given the size of their demand, not eliminating their exposure to international price spikes, underscoring the urgent need for regional manufacturing, strategic reserves, and coordinated procurement to build resilience.

Brazil has also made an effort to increase domestic production, but the country still imports about 80-85% of the fertilizer used in the country.

The Russia–Ukraine war, which started in early 2022, has shown how quickly fertilizer markets can react. Between November 2019 and the first half of 2022, the average FOB price of key inorganic fertilizers surged from $256 to $941 per metric ton, representing a collective increase of approximately 267% above pre-COVID-19 levels.5 Although prices have since stabilized, they have not returned to pre-COVID-19 levels. Farmers face significantly higher input costs, while governments continue expanding subsidy budgets to cushion the shock and protect national food production.

Delayed procurement decisions and absent regional coordination translate into higher costs. Rising global prices reduce fertilizer use. Lower use leads to reduced yields. Reduced yields drive food prices upward. The lesson from previous market disruptions is clear: reactive responses are costly. Early coordination, supply assurance, and regional alignment are far more effective than emergency interventions after prices have already surged.

Lessons from COVID‑19 and the 2022 fertilizer shock are clear: early coordination and supply assurance reduce costs and stabilize markets. Reactive, uncoordinated responses raise fiscal burdens while failing to protect farmers.

We call for immediate, concerted action by governments, multilateral institutions, regional bodies, the private sector, and civil society to stabilize supply volumes, moderate price spikes, and guarantee fair, timely farmer access.

Therefore, we urge the following immediate priorities:

- Convene a Global Fertilizer Crisis Response Committee to align procurement, logistics, financing, and policy (IFDC, International Fertilizer Association, World Bank Group, African Development Bank, Asian Development Bank, Islamic Development Bank, African Union, and regional counterparts, the private sector, and civil society).

- Prioritize fertilizers as “strategic commodities without borders.” Implement temporary value-added tax (VAT)/duty exemptions and green‑lane customs for fertilizer and packaging materials.

- Leverage the African Continental Free Trade Area (AfCFTA) to unlock intra‑African fertilizer trade, building on the Africa Fertilizer and Soil Health Summit commitments.

- Secure strategic volumes now through framework agreements with regional producers (e.g., Nigeria, Egypt, and North Africa for urea; Morocco for phosphates) with option clauses at current prices; and create strategic reserves.

- Deploy finance at scale: Central bank liquidity swap lines for fertilizer importers, letter-of-credit guarantees, freight/insurance co‑pays, and working‑capital facilities for importers, blenders, and agro-dealers.

IFDC, Sustain Africa, and AfricaFertilizer stand ready to support global or regional initiatives to implement the above recommendations.

In this context, existing crisis-monitoring platforms within IFDC, such as AfricaFertilizer and Sustain Africa’s crisis response mechanisms, will provide a proven foundation for coordinated monitoring and response. During the COVID-19 pandemic and the 2022 fertilizer market disruption, these initiatives combined market intelligence, country-level data, and stakeholder coordination to track supply flows, identify bottlenecks, and inform rapid policy responses across Africa.

These platforms can again provide regular market intelligence updates on fertilizer prices, supply disruptions, trade flows, and farmer access, enabling governments, development partners, and the private sector to anticipate shortages and coordinate procurement or policy measures.

- Argus Media daily alerts, March 2026 ↩︎

- Reuters: https://www.reuters.com/business/energy/us-oil-prices-jump-supply-fears-amid-expanding-us-israeli-war-with-iran-2026-03-08/ ↩︎

- IFA Market Intelligence Service, June 2025 ↩︎

- https://www.kpler.com/blog/global-fertiliser-dependency-on-gulf-exports-what-if-hormuz-is-disrupted ↩︎

- https://africafertilizer.org/#/en/results-and-data/price-statistics/ ↩︎