The next fertilizer crisis is inevitable.

Whether it becomes a food crisis depends on what we invest in now.

Geopolitical Risk Escalation and Global Market Disruptions

The growing geopolitical tensions between Israel, the United States, and Iran have created major uncertainty in global fertilizer markets, with Africa being especially vulnerable due to its structural reliance on imported fertilizers for agricultural production. The Strait of Hormuz is at the heart of the disturbance, as this waterway is used to transport a significant portion of the world’s ammonia and liquefied natural gas (LNG), both critical inputs for nitrogen fertilizer manufacture.

Widely traded finished fertilizers, such as urea, diammonium phosphate (DAP), and monoammonium phosphate (MAP), also transit through this route. The fertilizer industry has consistently pointed to rising freight and insurance costs, shipment delays, and increasing supplier risk aversion as immediate consequences of the conflict.

While physical shortages are not yet prevalent, the combination of logistical interruptions and speculative market behavior is already tightening supply conditions and pushing prices upward.

In March, IFDC and its partners conducted a rapid inventory to estimate fertilizer supply gaps in selected countries. This information was shared to guide regional coordination and encourage countries to conduct detailed inventories. The African Union Commission (AUC) and the Economic Community of West African States (ECOWAS) will lead the follow-up with their member countries.

Cross-Regional Risk Patterns

When comparing supply gaps to fertilizer demand, a consistent pattern appears across all regions. Countries with strong demand and heavy import dependency face the greatest immediate risk, especially when supply shortages exceed 30% of the national requirement. Medium-risk countries often have supply gaps of 15-30%, whereas low-risk countries either have smaller gaps or are now outside of the peak demand period.

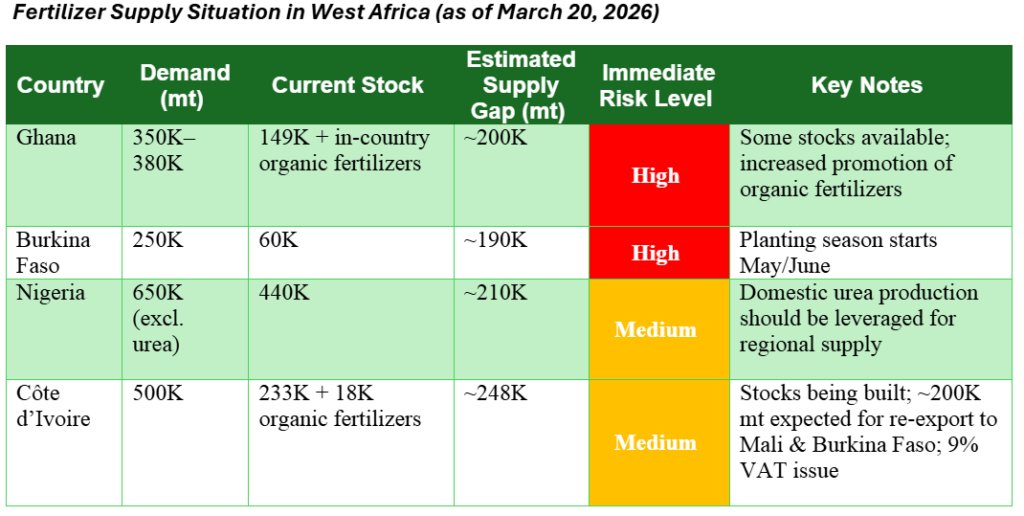

West Africa: Immediate Exposure and High Import Dependency

The impact of this situation on West Africa is both immediate and severe due to the region’s reliance on fertilizer imports and the timing of its agricultural seasons. Burkina Faso, Côte d’Ivoire, Ghana, and Senegal are among the countries that experience moderate to high fertilizer demand, typically ranging from 200,000 to 650,000 metric tons a year.

Current market signals and data indicate that supply deficits are emerging, driven by cautious procurement strategies among importers and delayed shipments. Urea’s vulnerability is exacerbated by its robust supply chain connections to the Middle East.

Countries such as Burkina Faso and Senegal are classified as high risk due to their import dependency and inadequate logistics systems. Ghana and Côte d’Ivoire are at medium to high risk, as the supply gaps are estimated to be substantial enough to disrupt the timely availability of fertilizer for farmers.

However, one country stands out in this context. Nigeria, a major urea producer, has decreased its own immediate vulnerability and offers the potential buffer to neighboring countries. Nigeria acts as a regional stabilizer due to its domestic urea production. Nonetheless, the country remains vulnerable to global trade disruptions, which can affect input costs, export logistics, and intra-regional distribution.

Landlocked Sahelian countries, such as Burkina Faso and Niger, are especially vulnerable to international and regional logistical disruptions because of their reliance on transit lanes.

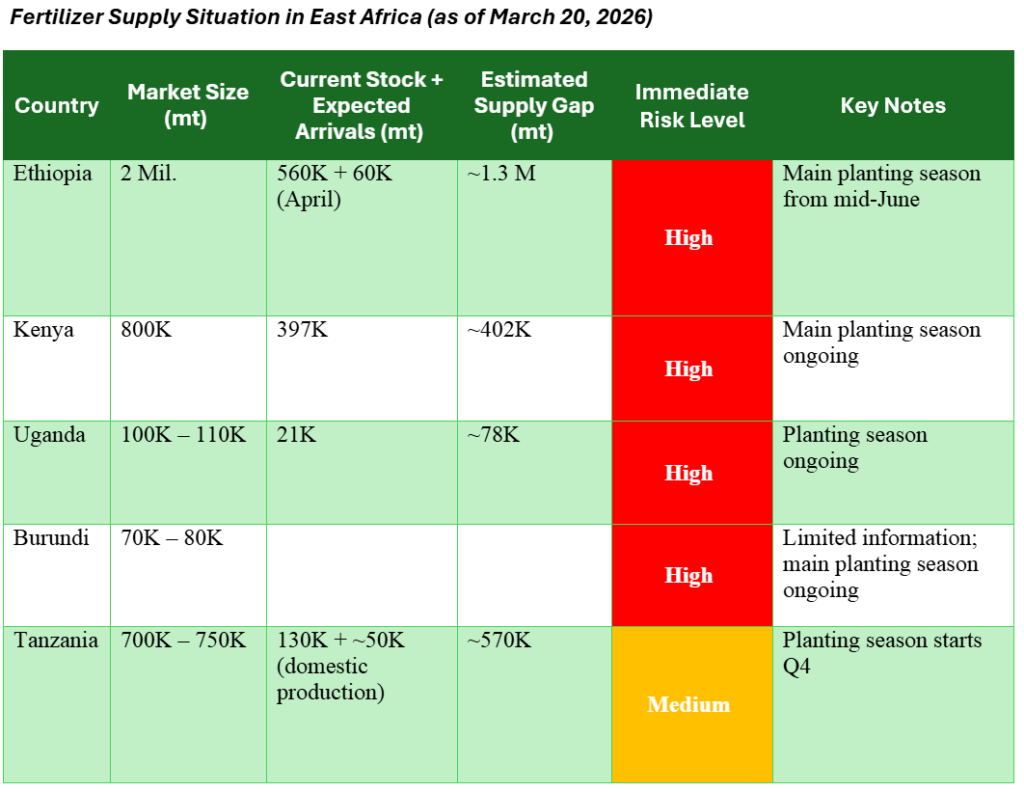

East Africa: Short-Term Stability, Rising Structural Risks

In East Africa, the situation remains relatively steady in the short term, but the risks are progressively increasing. Fertilizer demand in countries such as Ethiopia, Kenya, Tanzania, and Uganda is high and expanding due to staple crop output and government-sponsored input subsidy programs. In many countries, the procurement process for the current season began early enough to provide some short-term protection against global interruptions.

However, Ethiopia stands out as having very high demand and moderate supply risk, putting the country in the medium- to high-risk category. Uganda is under comparable difficulties due to its reliance on imports and weak demand levels. Kenya and Tanzania are better positioned in the short term, but they remain vulnerable if interruptions continue into the next procurement cycle.

Call to Action

The current fertilizer crisis requires timely, concerted efforts to protect agricultural production and food security.

IFDC, Sustain Africa, and AfricaFertilizer call for the following priority actions:

Medium–Term Actions

- Build market resilience by diversifying supply sources, prioritizing regional nitrogen and phosphate production.

- Establish strategic fertilizer and food reserves.

- Facilitate long‑term offtake agreements.

- Strengthen logistics, distribution systems, and infrastructure.

- Align fertilizer support with soil health and climate‑smart practices.

Long–Term Actions

- Build structural resilience through Investment in local and regional mineral and organic fertilizer production.

- Scale green ammonia and sustainable fertilizer pathways.

- Accelerate implementation of the Lomé and Nairobi Fertilizer Declarations.

- Embed fertilizer resilience into national food security and industrial strategies.

- Shift from crisis response to a resilient fertilizer system.

Disclaimer

This analysis is based on information compiled from multiple publicly available sources and market intelligence. While every effort has been made to verify the accuracy of the information, the authors and publishers accept no liability for any loss, damage, or disruption caused by errors, omissions, or the use of this information.

Sources: