Written by Sebastian Nduva, Lead, AfricaFertilizer.org; and Charlene Migwe, Senior Consultant, Development Gateway / Posted Courtesy of Fertilizer Focus

AfricaFertilizer.org (AFO), an initiative of the International Fertilizer Development Center (IFDC), has been tracking fertilizer-specific data sets in sub-Saharan Africa, including data on trade (import/exports), fertilizer production, distribution and flow of fertilizers, consumption, and policy around fertilizer markets. The AFO has partnered with Development Gateway, a subsidiary of IREX, to develop dashboards and tools to better manage and visualize fertilizer data in Africa. The partnership has launched dashboards for Kenya, Ghana, and Nigeria and is currently expanding to Zambia, Mozambique, Ethiopia, Senegal, and Malawi.

Correlation of logistics and fertilizer price

Agriculturally centred economies, such as those in the East Africa region, rely heavily on an efficient logistics network. Contributions from agriculture account for about 30% of the gross domestic product (GDP) in East African countries, with about 60-70% of the entire workforce reliant on agricultural activities. A robust system for tracking agro-input supply, including fertilizers, and farm produce distribution is key to the sustainability of this sector.

Fertilizer logistics, especially road transportation costs, constitute a significant component of fertilizer prices. This becomes even more important for landlocked countries dependent on their coastal neighbours.

Agriculturally centred economies rely heavily on an efficient logistics network

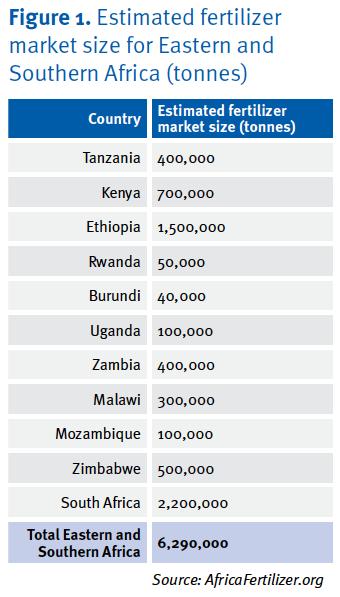

The major ports in East and Southern Africa through which fertilizers are shipped into the region include those of Djibouti, Mombasa, Dar es Salaam, Beira, Durban, and Cape Town. These ports serve 11 key fertilizer markets in the region, accounting for about 5-6 mn t of product, or about 60% of the entire sub-Saharan Africa fertilizer market. The ports of Durban and Djibouti account for the biggest share, with a combined total of 59% of the region’s fertilizer import needs, or about 3.7 mn t of fertilizer products.

Performance indicators

According to the 2018 World Bank Logistics Performance Index, which compares six key indicators – efficiency of the clearance process, quality of infrastructure, ease of arranging competitively priced shipments, competence and quality of logistical service, ability to track and trace consignments, and timeliness of shipments – Southern African ports lead the region, followed by those of Kenya and Tanzania.

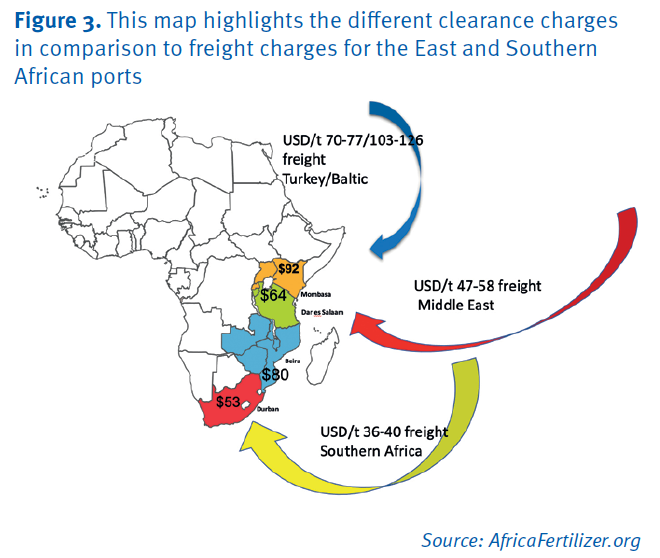

For the fertilizer sector, the main determinant of port choice is distance (geographical location) between the port and the supply destination, quality of connecting roads along the corridor and port infrastructure. Importers in landlocked countries, such as Rwanda or Burundi, have the option of importing fertilizer through the port of Mombasa in Kenya or Dar es Salaam in Tanzania, largely determined by the port costings as well as inland logistics to get the cargo to their supply centre.

Some importers in Southern African countries will sometimes opt to use Durban or Cape Town ports due to the congestion usually experienced at the port of Beira in Mozambique. The crisis in Eastern Europe has further exacerbated the situation, with freight indications doubling on most trade routes for fertilizer into the region. In 2021, the freight cost for a mid-size or large handysize fertilizer vessel (25,000-35,000 t deadweight tonnage) from the Middle East to East Africa was about USD25-30/t. This is up 48% as of the first quarter of 2022. The cost for a comparative vessel size from the same source to a Southern African port is up 30%. Freight rates from the Baltic to East Africa are up 50-60%. This increment in logistical cost has had a direct impact on fertilizer prices, which must be passed on to the farmers.

The increment in logistical costs have had a direct impact on fertilizer prices, which will be passed on to the farmer

Providing solutions

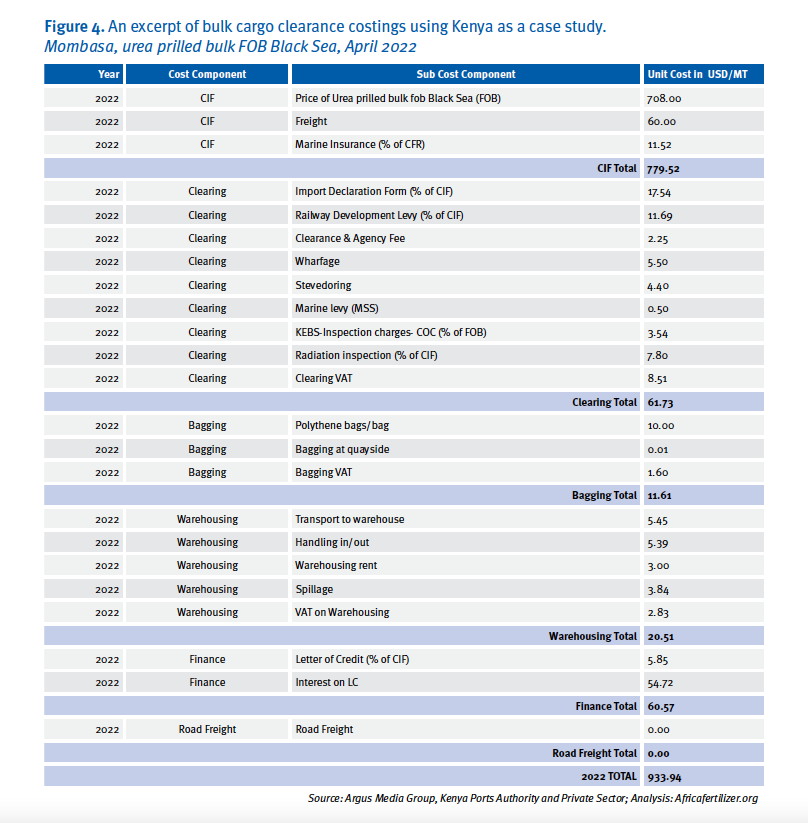

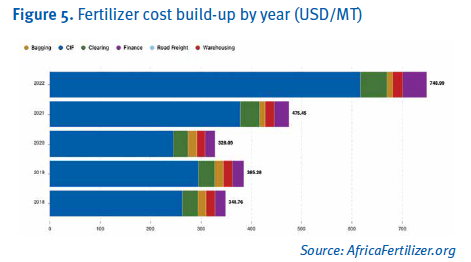

From the calculations in figure 4, moving fertilizer from international markets to Kenya costs around USD50/t. Additionally, it costs USD92/t to move the product inland. This clearly shows the influence of logistical costs as a significant function on the overall fertilizer price to farmers.

Some of the dashboards and market information systems developed by organizations such as IFDC are providing solutions to inform temporal and spatial management issues with regard to fertilizer movement in sub-Saharan Africa. These are providing transparency to the sector, thus enabling governments and private market actors to respond to the everchanging fertilizer landscape.

Current realities

Since the second quarter of 2021, global fertilizer prices have drastically increased. This has been driven by various factors, primarily the increase in natural gas prices and firm freight levels.

In June 2021, natural gas was trading at USD3.1/MMBtu. As of October 2021, the price was at USD6.3/ MMBtu, representing a 50% increase in less than five months. Natural gas accounts for more than 95% of ammonia tonnage, with 76% of all global ammonia used for fertilizer production.

In the first quarter of this 2022, the Russian invasion of Ukraine further compounded the situation, with vessels out of the Baltic region completely cut off, economic sanctions on Russia resulting in a strengthened US dollar, and unavailability of fertilizer for export from the region. All of these factors have significantly contributed to the average prices reaching a 10-year high.

The overall firmness of landed costs and unavailability of fertilizer in East and Southern Africa, and by extension the sub-Saharan Africa region, will continue for the foreseeable future, with freight/logistics costs, availability and affordability from global sources, and the Eastern European crisis being the biggest drivers of this current reality.