The next fertilizer crisis is inevitable.

Whether it becomes a food crisis depends on what we invest in now.

Escalating disruptions to global shipping related to the Middle East conflict are sharply increasing freight, fuel, and insurance costs, with direct consequences for fertilizer markets and food systems. While free-on-board (FOB) fertilizer prices continue to rise, elevated energy, transport, and insurance costs are keeping landed prices high in import-dependent regions.

This dynamic threatens farmers’ ability to afford agricultural inputs, raises food production costs, and heightens risks to agricultural output, food prices, and overall food security.

Shipping Disruptions and Cost Pressures

Since late February, freight rates for oil tankers have increased by more than 90%, while bunker fuel prices have nearly doubled. War risk insurance premiums have risen sharply, and in some cases, insurers have suspended coverage altogether for vessels operating in high-risk areas of the Persian Gulf.

As a result, shipowners are confronting difficult operational decisions. Many must either suspend services along the affected trade routes or operate under substantially higher insurance and fuel costs. In several corridors, insurance premiums have increased on a per voyage basis, compounding overall maritime transport expenses.

Price Transmission to Fertilizer Markets

Fertilizers are especially sensitive to shipping disruptions due to their bulk and geographic concentration of production. Nitrogen fertilizers are largely produced in energy-rich regions due to their dependence on natural gas, while phosphate and potash fertilizers are concentrated in countries with significant mineral reserves. Demand, however, is concentrated in import-dependent economies across Africa, South Asia, and parts of Latin America.

Rising energy, logistics, and insurance costs are now being transmitted into fertilizer markets, given the sector’s dependence on fuel-intensive production and long-distance trade. Higher energy and transport costs increase the landed price of fertilizers, thus raising the cost of agricultural inputs and ultimately affecting farmers’ production decisions.

The impacts build over time rather than taking effect immediately. As fertilizer prices rise, farmers reduce application rates, switch to crops that are less input‑intensive, or scale back planting – responses that result in lower yields and declining agricultural output in subsequent seasons.

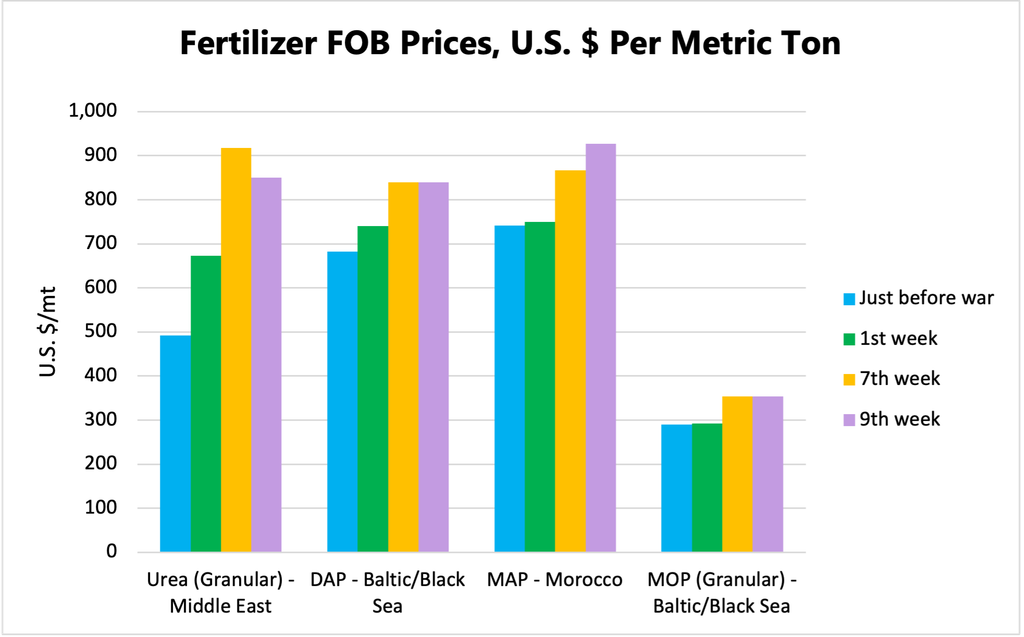

Fertilizer Price Response to the Shock

Market data shows a clear increase in international benchmark FOB prices across various categories of fertilizer since the beginning of the conflict.

Granular urea from the Middle East has registered the sharpest movement, increasing by 37% in Week 1, peaking at 86% by Week 7 at around U.S. $918 per metric ton (mt), before easing to 73% by Week 9 at approximately U.S. $850/mt.

Phosphate fertilizers have shown more moderate but sustained increases. Diammonium phosphate (DAP) from the Baltic region rose by 8% in Week 1, reached 23% by Week 7, and remained broadly stable through Week 9 at around U.S. $840/mt. Monoammonium phosphate (MAP) from Morocco increased from 1% in Week 1 to 17% by Week 7 and further to 25% by Week 9 at approximately U.S. $925/mt.

Potash markets also continue to trend upward, with muriate of potash (MOP) from the Baltic region increasing from 1% in Week 1 to 22% by Week 7 and stabilizing through Week 9 at around U.S. $354/mt.

While the magnitude varies by product, the overall trend indicates sustained upward pressure in fertilizer prices. However, these FOB price movements likely understate the full impact on importing countries. When combined with substantial increases in freight and insurance costs, the landed cost of fertilizers is rising more sharply, placing additional pressure on import-dependent markets.

Evidence from Fertilizer Shipping Markets

Recent shipping data highlights the scale of the disruption in fertilizer logistics. Freight costs have risen significantly across major routes between January and April:

- For fertilizer shipments of 15,000 to 20,000 mt, rates increased by about 40% (from U.S. $78/mt to U.S. $109/mt) on the Baltic to East Africa route and by approximately 677% (from U.S. $26/mt to U.S. $202/mt) on Middle East routes.

- For larger 40,000 mt shipments, rates rose by about 13% (from U.S. $70/mt to U.S. $79/mt) on the Baltic to South Africa route and by approximately 639% (from U.S. $23/mt to U.S. $170/mt) on Middle East routes.

These increases are particularly significant for fertilizers, which are typically transported in bulk and are highly sensitive to maritime costs. For many importing countries, such increases translate directly into higher retail and farm-gate prices, even in the absence of further increases in international benchmark prices.

Macroeconomic and Policy Implications

The broader macroeconomic implications are increasingly evident. According to the World Bank, rising commodity prices linked to the conflict are expected to increase inflation while constraining economic growth, particularly in developing countries.

Fuel pricing dynamics also shape how these shocks are transmitted domestically. In countries with liberalized fuel markets, retail fuel prices tend to adjust quickly, amplifying the immediate impact on transport and input costs. In contrast, countries with regulated pricing systems may delay adjustments, although government interventions to cushion consumers often place additional pressure on public finances.

For fertilizers, these dynamics influence both the cost of distribution and the affordability of inputs at farm level, further shaping agricultural outcomes.

Implications for Food Production and Imports

Persistently high landed fertilizer prices pose clear risks to agricultural production and food security. As fertilizer affordability declines, farmers may reduce application rates, change crop choices, or downsize their planted area. These adjustments can lower yields and tighten domestic food supplies.

For countries already dependent on food imports, reduced domestic production will likely increase import requirements at a time when global food prices and shipping costs are also rising. This creates a double burden: higher fertilizer import bills and higher food import bills, intensifying pressure on foreign exchange reserves and fiscal balances.

The result is heightened exposure to food price inflation and increased vulnerability to food insecurity, particularly in economies with limited capacity to absorb external shocks.

As highlighted in previous Fertilizer Crisis Response Bulletins, timely and coordinated policy action remains critical. Ensuring access to fertilizers, mitigating logistics constraints, and protecting farm input affordability will be essential to prevent the current shipping and energy disruptions from translating to sustained declines in agricultural production and longer term food security challenges.

Disclaimer

This analysis is based on information compiled from multiple publicly available sources and market intelligence. While every effort has been made to verify the accuracy of the information, the authors and publishers accept no liability for any loss, damage, or disruption caused by errors, omissions, or the use of this information.

Sources

![Farmers in Kenya spread organic fertilizer, developed by MIT spinout Safi Organics, to help improve the yield of their farmlands. [Safi Organics]](https://ifdc.org/wp-content/uploads/2026/08/MIT-Safi-Organics-01-press_0-350x240.jpg)