The next fertilizer crisis is inevitable.

Whether it becomes a food crisis depends on what we invest in now.

Contact Us Today

Status of the War in the Middle East

Geopolitical tensions between the United States, Israel, and Iran continue to create uncertainty in global trade and energy markets, especially around the Strait of Hormuz, a major shipping route for oil and fertilizers.

While direct conflict risks have eased somewhat due to ongoing diplomatic talks,1 markets remain cautious. Fertilizer supply chains are particularly sensitive, as prices depend heavily on energy costs, freight rates, and shipping reliability, all of which have been disrupted by the instability in the region.

Overall, the situation is contributing to continued volatility and risk premiums in global commodity and fertilizer markets, even without active escalation.

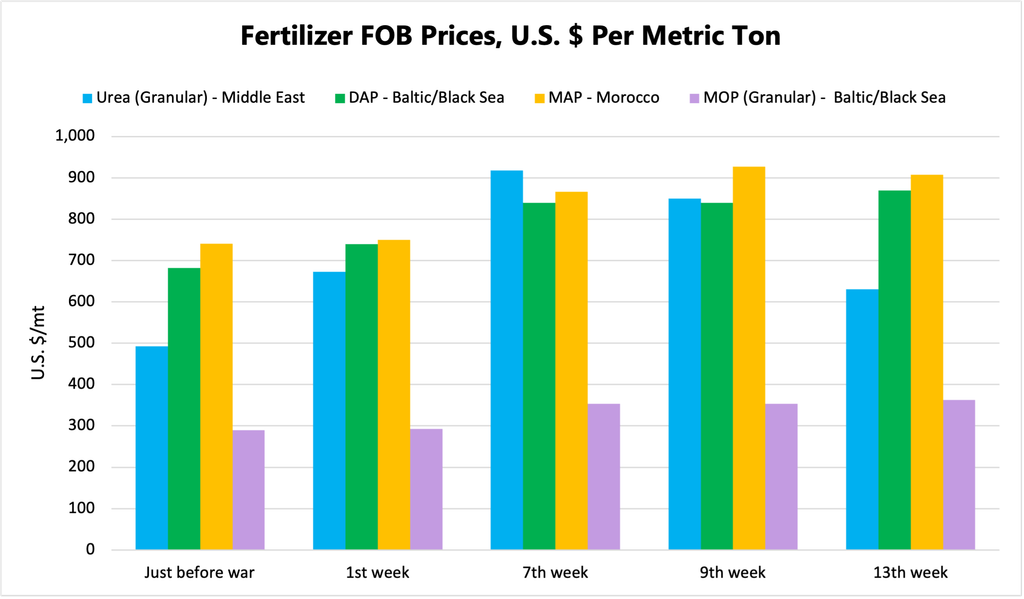

Global Fertilizer Market Update

Market data shows a clear increase in international benchmark free on board (FOB) prices since the beginning of the conflict.

Fertilizer markets remain elevated overall, but trends differ by product.

Middle East urea prices have fallen from earlier peaks to about U.S. $630 per metric ton (mt) as of Week 13, though this is still 28% above the pre-war level. Phosphate fertilizer prices remain high and stable: diammonium phosphate (DAP) has fluctuated slightly around U.S. $869-875/mt, while monoammonium phosphate (MAP) has remained firm at around U.S. $907-927/mt.

Potash prices have risen steadily, with muriate of potash (MOP, Baltic/Black Sea) increasing from U.S. $354/mt (Weeks 10-11) to U.S. $363/mt by Week 13, reflecting gradual market strengthening.

Overall, fertilizer markets remain 22-28% above pre-war levels. Urea pricing is easing after early peaks, phosphates are stable but elevated, and potash continues a slow upward trend.

East Africa

Uganda is advancing fertilizer adoption through a new partnership with Green Hydrogen Fertilizer Company (GHFC),2 focusing on farmer training and improved extension services, while maintaining strong import volumes of about 50,000 mt in early 2026.

Tanzania continues to manage fertilizer affordability and market stability through the Tanzania Fertilizer Regulatory Authority (TFRA), which focuses on regulating quality, raising awareness of nutrients in fertilizers,3 and overseeing pricing and distribution.4 Urea averages about 123,323 Tanzanian shillings (TSh) per 50-kg bag, with a 32% government subsidy, though actual prices vary by region due to transport costs, ranging from about TSh 69,240 in Dar es Salaam to TSh 78,020 in Tanga.5 Overall, the subsidy program remains central to cushioning farmers from global fertilizer price volatility during the 2026 agricultural season, even as internal logistics continue to drive notable regional price differences.

Ethiopia is expanding its fertilizer capacity, with Dangote Group increasing investment in the Gode plant from U.S. $2.5 billion to U.S. $4 billion, targeting 3 million mt of annual urea production6 and securing near-term supply through upcoming shipments.

In Kenya, fertilizer imports reached about 400,000 mt early in 2026, but trading has slowed post-planting season and uncertainty over NPK deliveries from Chinese suppliers continues.

Rwanda’s 2026A and 2026B fertilizer seasons experienced continued strong government support, with subsidies covering about 32% of urea and 41% of NPK 17-17-17 under indicative prices of 1,190 Rwandan francs (RWF) per kilogram and 1,369 RWF/kg, respectively. The Ministry of Agriculture is currently finalizing revised pricing and subsidy levels for the 2027A season (July-December), with an official announcement expected on July 1, 2026.

Southern Africa

South Africa is seeing weaker demand and slightly softer prices, with improved supply expected from incoming shipments.

Malawi remains vulnerable to supply disruptions due to import dependence and rising logistics costs, raising concerns about affordability and availability ahead of the next season.7

Mozambique has implemented an emergency input support program (April-June 2026), backed by the World Bank, distributing about 8,000 mt of free fertilizer (NPK and urea) to over 160,000 farmers across six provinces, with allocations based on cultivated land to support the current season.

In Zambia, the new United Capital Fertilizer (UCF) urea plant is improving local supply and regional distribution, including a planned hub in the Eastern Province to serve domestic demand and exports to Mozambique and Malawi. Local urea prices range from 1,000 to 1,200 Zambian kwacha per 50-kg bag, supporting affordability while strengthening regional supply chains.

Overall, regional markets show a mix of production capacity expansion, post-season demand slowdown, and continued subsidy-driven efforts to maintain affordability amid supply risks.

West Africa

At the regional level, the Economic Community of West African States (ECOWAS) extraordinary meeting of Ministers of Agriculture, held on March 23, 2026, directed the creation of a regional joint fertilizer purchasing system, moving away from fragmented national procurement. Since then, ECOWAS has consolidated member state fertilizer stock and demand data, drafted an implementation framework, and begun engaging regional suppliers, such as the Dangote Group and Indorama Corporation, to secure emergency supply. Financing is being structured through the ECOWAS Bank for Investment and Development (EBID) and the West African Development Bank (BOAD), using guarantees and escrow-backed trade finance to reduce risk and stabilize procurement.

Ghana is rolling out a phased fertilizer procurement plan to support the 2026 free fertilizer distribution policy, with an initial allocation of about 25,000 mt of urea and NPK for the main planting season, which began in April. A second tranche is planned for the northern season, amid concerns over whether total supply and timing will fully meet national demand.

Benin is maintaining fertilizer subsidies at about 31.8 billion West African CFA francs (FCF)8 to keep prices stable despite global market pressure. Under the program, urea is fixed at FCFA 15,000 per 50-kg bag compared to an estimated market price of FCFA 19,250, while NPK fertilizers for both cotton and food crops remain at FCFA 17,000 per 50-kg bag against market prices of FCFA 23,500 and FCFA 24,250, respectively.

Niger received a donation of 20,000 mt of fertilizer from Russia to support agricultural production and strengthen food security for the 2026 season.9

Burkina Faso has introduced input subsidies for the 2026 agricultural campaign, setting NPK and urea at 15,000 FCFA per 50-kg bag for smallholder farmers and 17,000 FCFA for larger producers to maintain affordability amid rising global prices.10 In addition, the government is extending support to complementary inputs such as certified seeds and organic fertilizers at fixed prices, as part of a broader effort to stabilize input markets and safeguard farmer access despite ongoing volatility.

Nigeria is experiencing significant fertilizer price increases despite relatively low demand at the start of the planting season, with urea rising by about 43% from 35,000 Nigerian naira (₦) per 50-kg bag in February to ₦50,000 in May. NPK prices also increased, with NPK 20-10-10 rising by about 12% from ₦43,000 to ₦48,000 per 50-kg bag, driven by global market uncertainty, foreign exchange pressures, higher natural gas costs, and increased import costs for key raw materials, such as DAP and MOP.

Togo’s fertilizer availability for the 2026/27 agricultural season remains adequate, supported by strong carryover stocks and planned imports, with total stocks at about 111,800 mt as of April 2026, including over 52,000 mt of urea and 58,000 mt of NPK 15-15-15. Fertilizer prices remain stable at FCFA 18,000 per 50-kg bag under the government subsidy program, while an additional 115,000 mt are expected to be imported to ensure continuous supply throughout the season.

Overall, the region is balancing coordinated procurement reforms, subsidy programs and emergency interventions to manage rising global fertilizer costs and supply uncertainty, while maintaining farmer access and market stability across countries.

Disclaimer

This analysis is based on information compiled from multiple publicly available sources and market intelligence. While every effort has been made to verify the accuracy of the information, the authors and publishers accept no liability for any loss, damage, or disruption caused by errors, omissions, or the use of this information.

Sources

- Iranian delegation in Qatar as talks on US ceasefire extend ↩︎

- Uganda Partners with GHFC to Boost Fertiliser Use and Agricultural Productivity ↩︎

- Tanzania: TFRA Shifts Farmers’ Focus to Fertiliser Quality ↩︎

- TFRA warns fertiliser agents over violations in Kilimanjaro ↩︎

- Tanzania: Fertilizer Indicative Prices 2026 ↩︎

- Dangote Expands Investment in Ethiopia’s 3 Million-Ton Fertilizer Project to $4 Billion ↩︎

- Gulf shipping standoff hits Africa’s most vulnerable farmers ↩︎

- 2026-2027 Agricultural Season: Subsidies of over 31 billion FCFA for fertilizer in Benin ↩︎

- Russia donates 20 000 tonnes of mineral fertilisers to Niger ↩︎

- Burkina Faso: The Ministry of Agriculture sets fertilizer prices for small-scale producers ↩︎

![Farmers in Kenya spread organic fertilizer, developed by MIT spinout Safi Organics, to help improve the yield of their farmlands. [Safi Organics]](https://ifdc.org/wp-content/uploads/2026/08/MIT-Safi-Organics-01-press_0-350x240.jpg)